In our view, markets are being driven by two key factors that are to a degree interwoven: the clear strength of the global economies which are driving diversification towards non-tech/AI trades; and significant levels of uncertainty and confusion around the AI trade. Regardless of what market commentators claim to know about AI and the investment cycle, it is purely conjecture and the only certainty is that there is no certainty. Markets hate uncertainty and so volatility is picking up, and investors are being buffeted by strong investment winds. The reaction has been to move into safer havens.

Looking at the rotation in tech – software versus hardware and beyond

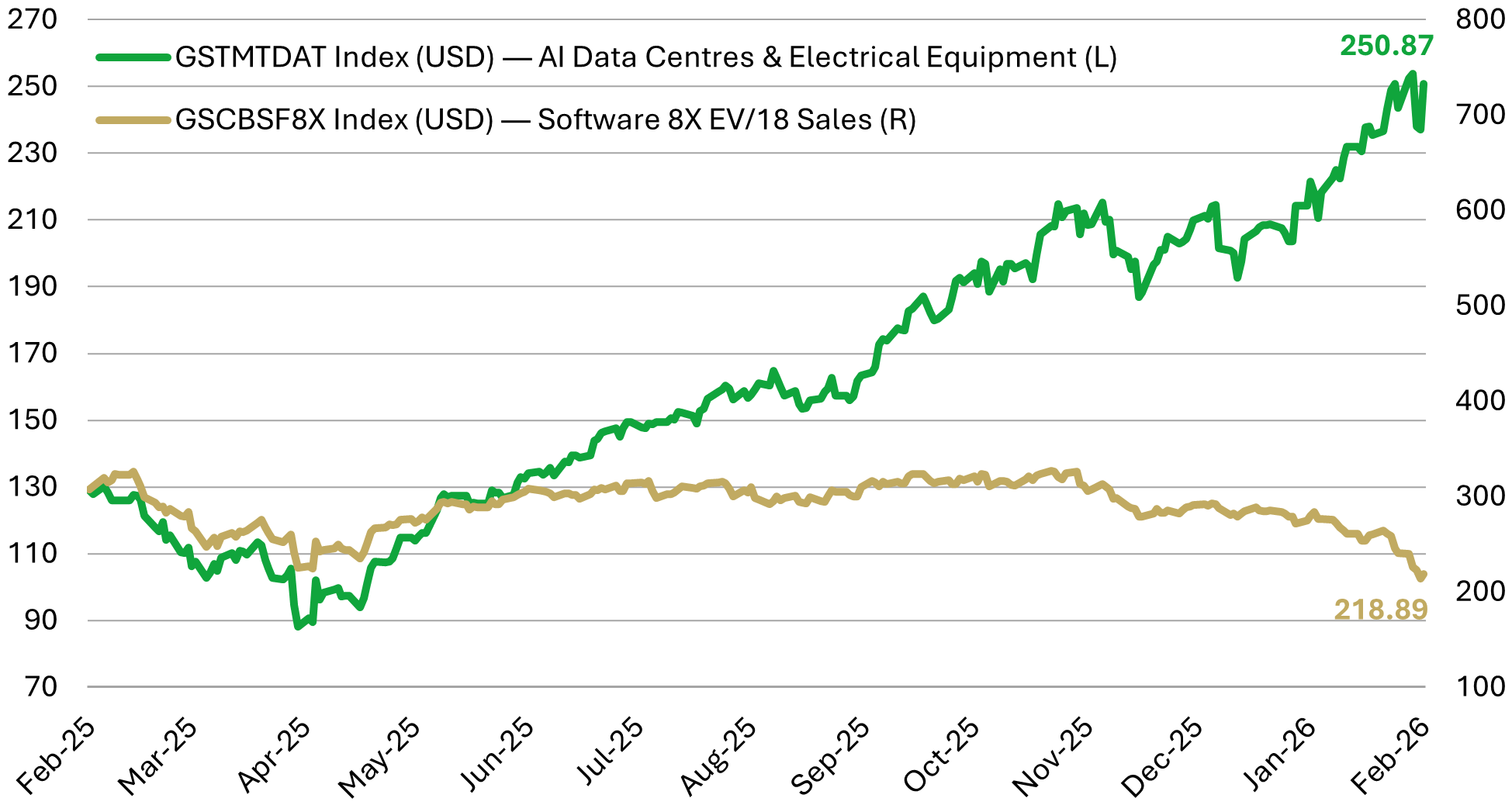

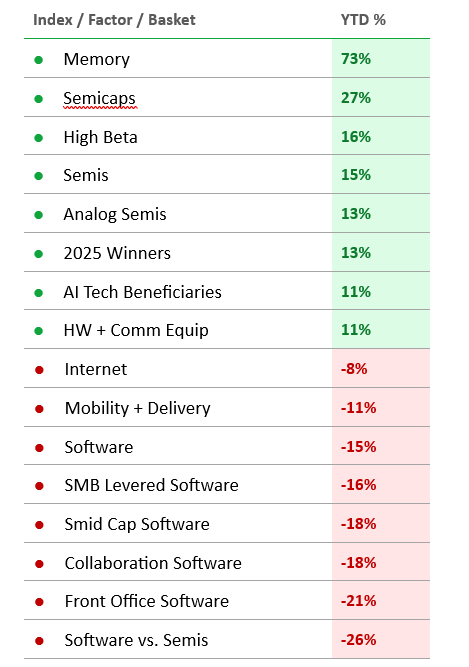

The following charts highlight the most visible element of the rotation and pain trade within technology that has been accelerating this year – hardware versus software, using the Goldman Sachs (GS) baskets for AI Hardware and Expensive Software for the last 12 months and a factor performance table for the year to date.

Software has been under pressure for almost a year in relative terms and the end of 2025 and start of 2026 has seen this accelerate. The reason for the moves has been attributed to the belief that AI will eat software, or that much traditional software will become totally redundant as it is replaced by AI products spun up at a moment’s notice to create proprietary systems to handle everything from HR to CRM.

We believe that fundamentally this is impossible to envisage. Corporate software systems are complex, not only in the software itself but also the protocols surrounding that software. Enterprises require enterprise level service agreements, and they rely on brands and customer support.

Source: Bloomberg, 12 months to 6 February 2026.

Source: Jefferies, 2 February 2026. YTD = Year to date.

There is no doubt that AI will have a profound impact on the creation of code but the notion that traditional software will be replaced is fanciful. Jensen Huang of Nvidia made this very point at the Cisco Ai summit on 3 February. He raised the important question of whether we want to use tools or reinvent them. His answer was: "The notion that AI is somehow going to replace software companies is the most illogical thing in the world, and time will prove itself."

Bill McDermott, CEO of ServiceNow, reinforced this view in a recent earnings call, saying: "The speculation that AI will eat software companies is out there. Let's clear it up with the facts. Enterprise AI will be the largest driver of return on the multi-trilliondollar super-cycle of investment in AI infrastructure. The real payoff comes when trillions of tokens move beyond pilots to be embedded directly into the workflows where business decisions are made."

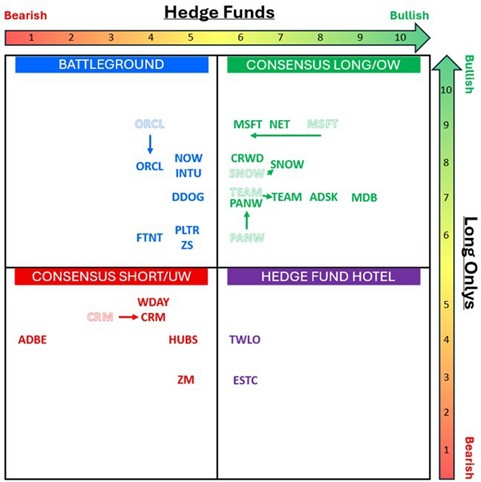

The following chart shows current positioning in the markets. We believe the consensus underweights bucket contains names that will in time show themselves to have been very cheap at around 4 times revenues. The CEO of Salesforce went on a buying spree in 2016 when software was in the doldrums and valuations of 4 times revenue were on offer, often seen as a line in the sand for software valuation.

The Software Sentiment Matrix:

(Last updated 27.01.26)

Source: Schilsky’s Software Sentiment Matrix, JP Morgan, as of February 2026.

To further drive home the momentum trade into AI winners and losers, the market last week started to heavily punish companies that use data sets to drive subscription models. The catalyst for this latest move was the launch of Claude and the legal plug ins that were released allowing for access and management of legal datasets.

It doesn’t matter how clever AI is, it can only work with the data it is given or it can access. So, the defining barrier to entry, as we have always said, is the data itself. If AI can access the data, the competitive threat is real; but if the data is proprietary, it is not. For example, S&P Global has a huge amount of proprietary data around its indices – AI can’t access this without paying for it and licensing it like any other paying customer. This is the framework for deciding who wins and who loses: who owns the data?

What will reverse this extreme

We are constantly asked when this trend will reverse. We use a proprietary T Score system to help us decide when to own names we like, how much to own and how to risk manage them. These indicators are still set firmly negative on software and positive on hardware. We will not add to software until our indicators change, thus avoiding the ‘catching a falling knife’ syndrome. However, we have a shopping list.

Some of the hardest hit software names like Workday, Adobe and Salesforce are trading around the 4x revenue level that we consider to be fundamentally cheap. At the same time, hardware names have been stratospheric and valuations are looking stretched. What we need is a catalyst. We think it is possible the latest round of mega scaler capex plans might deliver that catalyst, Capital spending plans have been pushed up across the board, with Google being the latest company to raise 2026 numbers from $120 billion to an expected $175-185 billion.

The first order response is likely to be that this is great for the hardware companies. Counter intuitively, we believe the opposite. The faster the capex numbers go up, the quicker we reach peak capex levels. Markets thrive on growth surprises: there is a huge difference between 100% growth split across two years versus 100% growth in year one and zero growth in year two. The second order derivative matters and so this might be a sign that capex names are close to the top for now. The counter side to this trade will be that software is close to the bottom. Time will tell!

KEY RISKS

Past performance does not predict future returns. You may get back less than you originally invested.

We recommend this fund is held long term (minimum period of 5 years). We recommend that you hold this fund as part of a diversified portfolio of investments.

The Funds managed by the Global Equities Team:

- May hold overseas investments that may carry a higher currency risk. They are valued by reference to their local currency which may move up or down when compared to the currency of a Fund.

- May encounter liquidity constraints from time to time. The spread between the price you buy and sell shares will reflect the less liquid nature of the underlying holdings.

- May invest in smaller companies and may invest a small proportion (less than 10%) of the Fund in unlisted securities. There may be liquidity constraints in these securities from time to time, i.e. in certain circumstances, the fund may not be able to sell a position for full value or at all in the short term. This may affect performance and could cause the fund to defer or suspend redemptions of its shares.

- May have a concentrated portfolio, i.e. hold a limited number of investments or have significant sector or factor exposures. If one of these investments or sectors / factors fall in value this can have a greater impact on the Fund's value than if it held a larger number of investments across a more diversified portfolio.

- May invest in emerging markets which carries a higher risk than investment in more developed countries. This may result in higher volatility and larger drops in the value of a fund over the short term.

Certain countries have a higher risk of the imposition of financial and economic sanctions on them which may have a significant economic impact on any company operating, or based, in these countries and their ability to trade as normal. Any such sanctions may cause the value of the investments in the fund to fall significantly and may result in liquidity issues which could prevent the fund from meeting redemptions. - May invest in companies predominantly in a single country which maybe subject to greater political, social and economic risks which could result in greater volatility than investments in more broadly diversified funds.

- May hold Bonds. Bonds are affected by changes in interest rates and their value and the income they generate can rise or fall as a result; The creditworthiness of a bond issuer may also affect that bond's value. Bonds that produce a higher level of income usually also carry greater risk as such bond issuers may have difficulty in paying their debts. The value of a bond would be significantly affected if the issuer either refused to pay or was unable to pay.

- May, in certain circumstances, invest in derivatives but it is not intended that their use will materially affect volatility. Derivatives are used to protect against currencies, credit and interest rate moves or for investment purposes. The use of derivatives may create leverage or gearing resulting in potentially greater volatility or fluctuations in the net asset value of the Fund. A relatively small movement in the value of a derivative's underlying investment may have a larger impact, positive or negative, on the value of a fund than if the underlying investment was held instead.

The risks detailed above are reflective of the full range of Funds managed by the Global Equities Team and not all of the risks listed are applicable to each individual Fund. For the risks associated with an individual Fund, please refer to its Key Investor Information Document (KIID)/PRIIP KID."

The issue of units/shares in Liontrust Funds may be subject to an initial charge, which will have an impact on the realisable value of the investment, particularly in the short term. Investments should always be considered as long term.

DISCLAIMER

This material is issued by Liontrust Investment Partners LLP (2 Savoy Court, London WC2R 0EZ), authorised and regulated in the UK by the Financial Conduct Authority (FRN 518552) to undertake regulated investment business.

It should not be construed as advice for investment in any product or security mentioned, an offer to buy or sell units/shares of Funds mentioned, or a solicitation to purchase securities in any company or investment product. Examples of stocks are provided for general information only to demonstrate our investment philosophy. The investment being promoted is for units in a fund, not directly in the underlying assets.

This information and analysis is believed to be accurate at the time of publication, but is subject to change without notice. Whilst care has been taken in compiling the content, no representation or warranty is given, whether express or implied, by Liontrust as to its accuracy or completeness, including for external sources (which may have been used) which have not been verified.

This is a marketing communication. Before making an investment, you should read the relevant Prospectus and the Key Investor Information Document (KIID) and/or PRIIP/KID, which provide full product details including investment charges and risks. These documents can be obtained, free of charge, from www.liontrust.com or direct from Liontrust. If you are not a professional investor please consult a regulated financial adviser regarding the suitability of such an investment for you and your personal circumstances.

Mark Hawtin

Mark Hawtin is head of the Global Equities team. Mark joined Liontrust in 2024 from GAM, where he was an Investment Director running global long-only and long/short funds investing in the disruptive growth & technology sectors. Before joining GAM in 2008 he was a partner and portfolio manager with Marshall Wace Asset Management for eight years, managing one of Europe’s largest technology, media and telecoms hedge funds.