View the latest insights from the Economic Advantage team.

VIew NowPast performance does not predict future returns. You may get back less than you originally invested. Reference to specific securities is not intended as a recommendation to purchase or sell any investment.

Key highlights

- The main detractors to Fund performance over the period were Mortgage Advice Bureau, GlobalData, Sage and Kainos within the Technology sector, with share price weakness driven by market concerns around AI disruption rather than any evidence of operational deterioration.

- Contributors from other sectors within a balanced portfolio provided valuable ballast against the negative sentiment impacting technology holdings, with healthcare giants GSK and AstraZeneca leading performance over the period.

- Rising geopolitical and economic risks reinforce the importance of the portfolio’s Quality attributes, with high returns on capital, high margins, strong solvency and earnings stability. Despite these attributes, the portfolio now trades at a weighted average free cash flow yield over 2 percentage points cheaper than the wider UK stockmarket, highlighting the ongoing extreme disconnect between company valuations and fundamentals.

Performance

The Liontrust Special Situations Fund returned 0.2%* in February. The FTSE All-Share Index comparator benchmark returned 6.5% and the average return in the IA UK All Companies sector, also a comparator benchmark, was 3.9%.

Commentary

In February, markets balanced solid equity gains with a rise in geopolitical risk. The FTSE 100 rose by 7.0%, with strength in energy, mining and defence names. The market’s relatively low exposure to the most expensive areas of global technology, alongside positioning that benefited from both the ongoing AI-related rotation and firmer oil prices, underpinned performance. Mid and small caps lagged comparatively, with the FTSE 250 up 2.3%, the FTSE Small Cap ex-IT rising 1.6% and the FTSE AIM All-Share gaining 0.4%. Expectations that UK inflation was continuing to ease also supported sentiment, reinforcing the prospect of further Bank of England rate cuts later in the year.

Globally, however, the backdrop became more unsettled toward month-end. Escalating tensions in the Middle East, including military strikes and disruption around the Strait of Hormuz, drove a sharp move higher in oil prices. This triggered more volatility in global equity markets moving into March.

The main detractors to Fund performance over the period were Mortgage Advice Bureau (-17%), GlobalData (-20%), Sage (-14%) and Kainos (-16%), with share price weakness driven by market concerns around AI disruption rather than any evidence of operational deterioration. We have devoted considerable time over the past few years to research, thought and debate over the impact of AI on all the companies we hold where there is a perceived theoretical or actual impact on their competitive advantage, either now or in the future. This is a nascent and evolving new technology, and we continue to challenge our working assumptions as material new developments emerge. The team has access to many technology company founders with whom we have extensively discussed the AI risks and opportunities facing our businesses. The team has also spoken with several software/technology analysts representing a range of views on AI and its potential impact.

We believe that the best-protected companies have broad and deep offerings that embed them within their end customers and/or ownership of proprietary data. Many of the portfolio companies provide “systems of record” that are integral to a customer’s operations; these are typically harder to replace than “systems of engagement”, which can be more vulnerable. Other supportive attributes include exposure to regulated end markets and a combination of hardware alongside software.

Starting with Mortgage Advice Bureau, the market concern is that AI-native advice tools reduce reliance on advisers, compressing volumes and pricing. We view that MAB’s defensibility is rooted in operating at scale in a highly regulated environment where suitability, accountability, record-keeping and governance matter, alongside handling complex, non-standard mortgage cases through robust workflows. We see AI more likely as a productivity lever (document processing, triage, scenario analysis), a view which was reinforced by a recent head office visit focused on the company’s technology roadmap.

GlobalData shares have trended down over the last year, with the move from AIM to the Main Market also a detracting factor, despite takeover interest from two parties in early 2025. Again, recent meetings and a site visit emphasised the defensibility of GlobalData’s layered proposition: hard-to-replicate proprietary datasets plus highly specialised analysis delivered through one platform. New AI tools have driven 2–3x higher platform usage, and the AI hub now serves 42,000+ users; margins reflect current investment with a stated expectation of improvement in 2026.

Sage is down ~23% year-to-date even though execution has been strong (consistent 9–10% organic ARR/revenue growth and mid-teens operating profit growth via margin expansion). The company positions AI as an opportunity, building on existing machine learning (ML) capabilities and expanding generative AI through Sage CoPilot and agents across compliance, reconciliation and tax. We believe Sage’s deep domain expertise, system-of-record status and strong accountant distribution channel remain powerful competitive advantages.

Kainos has sold off around 40% from its November peak. The bear case is that AI coding tools could reduce labour intensity within Digital Services; however, we see potential for faster, more cost-effective delivery to unlock additional demand, particularly in the under-digitised UK public sector. Kainos is already 65% AI-enabled on delivery, and healthcare revenue grew 33% in H1 FY26. Within the Workday-related divisions, we take comfort from Workday’s entrenched system-of-record position. While near-term share price performance has been influenced by Workday’s weakness, this has occurred despite an improving underlying trading backdrop at Kainos.

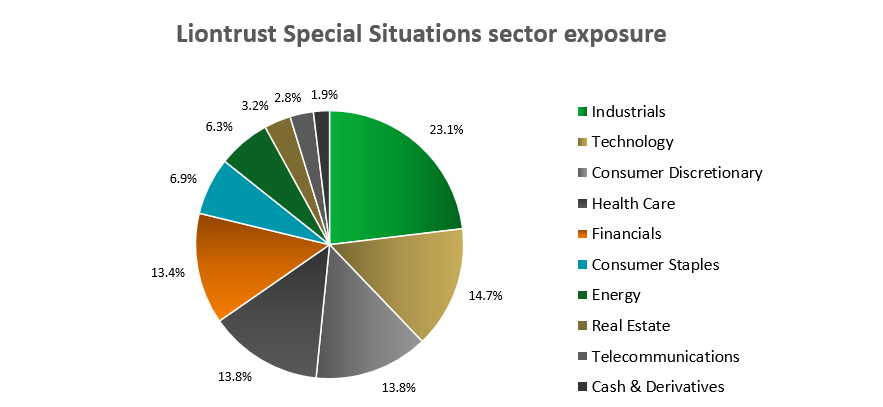

More broadly, it is important to note that portfolio construction is deliberately designed to limit over-exposure to any single stock (our risk-driven target weight discipline caps NAV exposure for the largest positions at 4%), and that the sector spread is broad. A 14.7% weighting to the technology sector at the end of February – while a significant overweight to the benchmark – remains well balanced in absolute terms by exposure to other sectors within the Fund.

Thus, contributors within other sectors for the Fund provided valuable ‘ballast’ in the face of the sentiment hit to the technology holdings during February. Healthcare giants GSK (+18%) and AstraZeneca (+15%) led the top performers for the period. GSK’s shares strengthened after the company reported full-year 2025 results showing solid revenue and profit growth, driven primarily by strong performance in its Specialty Medicines portfolio, including oncology, HIV and respiratory treatments. The results marked the first earnings update under new CEO Luke Miels, and management commentary emphasised continued commercial momentum and pipeline progress.

AstraZeneca also benefitted from a strong full-year 2025 results release, which demonstrated robust revenue growth and performance ahead of expectations, supported by strong demand across key therapy areas, particularly oncology. Management provided constructive guidance for 2026, highlighting ongoing pipeline advancements and sustained commercial momentum.

Shares in Renishaw (+13%), an engineering company focused on precision measurement and manufacturing technology, benefited following strong half-year financial results for the six months to 31 December 2025, which showed 7.1 % revenue growth and an 11 % increase in adjusted operating profit, reflecting solid momentum into the second half of the financial year. The market reacted positively to the improved profitability, expanding order book and the company’s optimistic earnings guidance for full-year 2026, with projected revenue and profit growth ranges that exceeded prior expectations.

Unilever’s (+11%) share price was supported by its full-year 2025 results, which delivered solid underlying sales growth and resilient operating margins, reflecting improved execution and cost discipline. Management also reaffirmed its medium-term growth ambitions and guided to continued sales growth and modest margin improvement in 2026.

Turning to the outlook, in an environment where volatility and uncertainty has spiked significantly due to the geopolitical situation in the Middle East, we remain convinced that the portfolio’s core Quality attributes are all the more valuable. The style factors of Value and Momentum have dominated investment returns in recent years, with a particularly punitive outperformance of the latter factor in 2025 and early 2026, in large part due to the overwhelming weight of relative flows into passive investment vehicles. However, Momentum is inherently a mean-reverting factor, and the extremity of current investor positioning and market concentration inevitably brings with it significantly elevated risks.

It is our firm belief that the attractions of our portfolio – with more than twice the cash flow return on capital of the wider UK market, higher margins, substantially lower leverage and evidence of strong earnings and sales growth stability over time – will ultimately ‘out’. It is all the more compelling when the valuation of the portfolio is viewed in the context of the Fund’s 20-year history: at a weighted average free cash flow yield of 8.6% (source: Style Analytics (28.02.26), the portfolio is not only cheaper than it has been since the height of the global financial crisis in 2008-9, but also more than two full percentage points cheaper than its benchmark, despite its Quality characteristics.

Borrowing from Benjamin Graham’s famous adage: the market’s ‘voting machine’ may be in full swing in the short term, but the opportunity presented by the long term ‘weighing machine’ has rarely, if ever, looked so compelling.

Positive contributors included:

GSK (+18%), AstraZeneca (+15%), Renishaw (+13%), Cohort (+12%) and Unilever (+11%).

Negative contributors included:

DotDigital (-22%), GlobalData (-20%), Mortgage Advice Bureau (-17%), Sage (-14%) and Kainos (-16%).

Discrete years' performance** (%) to previous quarter-end:

| Dec-25 | Dec-24 | Dec-23 | Dec-22 | Dec-21 |

Liontrust Special Situations I Inc | -3.8% | 2.9% | 6.3% | -11.2% | 20.5% |

FTSE All Share | 24.0% | 9.5% | 7.9% | 0.3% | 18.3% |

IA UK All Companies | 15.4% | 7.9% | 7.4% | -9.1% | 17.2% |

Quartile | 4 | 4 | 3 | 3 | 1 |

*Source: Financial Express, as at 28.02.26, total return (net of fees and income reinvested), bid-to-bid, institutional class. **Source: Financial Express, as at 31.12.25, total return (net of fees and income reinvested), bid-to-bid, primary class.

Understand common financial words and termsSee our glossary

KEY RISKS

Past performance does not predict future returns. You may get back less than you originally invested.

We recommend this fund is held long term (minimum period of 5 years). We recommend that you hold this fund as part of a diversified portfolio of investments.

- Overseas investments may carry a higher currency risk. They are valued by reference to their local currency which may move up or down when compared to the currency of the Fund.

- The Fund, may in certain circumstances, invest in derivatives but it is not intended that their use will materially affect volatility. Derivatives are used to protect against currencies, credit and interest rate moves or for investment purposes. The use of derivatives may create leverage or gearing resulting in potentially greater volatility or fluctuations in the net asset value of the Fund. A relatively small movement in the value of a derivative's underlying investment may have a larger impact, positive or negative, on the value of a fund than if the underlying investment was held instead.

- Credit Counterparty Risk: outside of normal conditions, the Fund may hold higher levels of cash which may be deposited with several credit counterparties (e.g. international banks). A credit risk arises should one or more of these counterparties be unable to return the deposited cash.

- Diversification Risk: the Fund is expected to invest in companies predominantly in a single country which maybe subject to greater political, social and economic risks which could result in greater volatility than investments in more broadly diversified funds.

- Liquidity Risk: the Fund will invest in smaller companies and may invest a small proportion (less than 10%) of the Fund in unlisted securities. There may be liquidity constraints in these securities from time to time, i.e. in certain circumstances, the fund may not be able to sell a position for full value or at all in the short term. This may affect performance and could cause the fund to defer or suspend redemptions of its shares.

- Smaller Companies Risk: the Fund may invest in companies listed on the Alternative Investment Market (AIM) which is primarily for emerging or smaller companies. The rules are less demanding than those of the official List of the London Stock Exchange and therefore companies listed on AIM may carry a greater risk than a company with a full listing.

- ESG Risk: there may be limitations to the availability, completeness or accuracy of ESG information from third-party providers, or inconsistencies in the consideration of ESG factors across different third party data providers, given the evolving nature of ESG.

The issue of units/shares in Liontrust Funds may be subject to an initial charge, which will have an impact on the realisable value of the investment, particularly in the short term. Investments should always be considered as long term.

DISCLAIMER

This material is issued by Liontrust Investment Partners LLP (2 Savoy Court, London WC2R 0EZ), authorised and regulated in the UK by the Financial Conduct Authority (FRN 518552) to undertake regulated investment business.

It should not be construed as advice for investment in any product or security mentioned, an offer to buy or sell units/shares of Funds mentioned, or a solicitation to purchase securities in any company or investment product. Examples of stocks are provided for general information only to demonstrate our investment philosophy. The investment being promoted is for units in a fund, not directly in the underlying assets.

This information and analysis is believed to be accurate at the time of publication, but is subject to change without notice. Whilst care has been taken in compiling the content, no representation or warranty is given, whether express or implied, by Liontrust as to its accuracy or completeness, including for external sources (which may have been used) which have not been verified.

This is a marketing communication. Before making an investment, you should read the relevant Prospectus and the Key Investor Information Document (KIID) and/or PRIIP/KID, which provide full product details including investment charges and risks. These documents can be obtained, free of charge, from www.liontrust.com or direct from Liontrust. If you are not a professional investor please consult a regulated financial adviser regarding the suitability of such an investment for you and your personal circumstances.